Planning your finances and choosing investments can be stressful especially when markets are volatile. But it can be downright scary when like in 2008 they enter free-fall. Many people have decided that the stress (and chance of loss) just isn’t worth it and so they have chosen to stay out of the market altogether. Unfortunately, that means that by the time they finally decide to return to the market it will probably be nearing another top and they will get hit with major losses once again.

This is not just a symptom of the perversity of human nature. It is also the nature of markets because as the market goes up it draws in more people who had been sitting on the sidelines but eventually there are no more people with money on the sidelines so as the last 10% of buyers (the most reluctant) enters the market it begins to top and finally there are no new buyers left and so the market begins crashing. As the old saying goes, “when the bag boy at the supermarket is talking about retiring on his stock market portfolio it is time to get out of the market.”

This is not just a symptom of the perversity of human nature. It is also the nature of markets because as the market goes up it draws in more people who had been sitting on the sidelines but eventually there are no more people with money on the sidelines so as the last 10% of buyers (the most reluctant) enters the market it begins to top and finally there are no new buyers left and so the market begins crashing. As the old saying goes, “when the bag boy at the supermarket is talking about retiring on his stock market portfolio it is time to get out of the market.”

Today Chris Ciovacco the Chief Investment Officer for Ciovacco Capital Management, LLC (CCM) looks at reducing investment stress. ~Tim McMahon, editor

Want to Reduce Investment Stress?

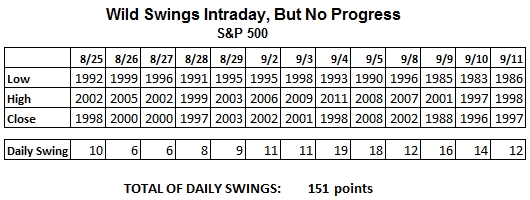

151 Point Energy-Sapping Move

If we told you the S&P 500 had moved 151 points since August 24, you would probably say, “you are crazy”. The S&P 500 closed at 1998 on August 25. The close on September 11 was just one point lower (1997). While the market has made little progress (up or down) since August 25, those who have been watching it tick-by-tick have gone on a 151 point energy-sapping and stress-inducing roller coaster ride. The table below shows the intraday swings on the S&P 500 dating back to August 25. The total of the intraday ups and downs comes to 151 points.

Focus On Closing Prices

For investors, watching the market tick-by-tick is often an unnecessary exercise. The real information concerning the net outcome between the bulls and bears comes in the form of the closing price. The same concepts apply to a weekly timeframe; the weekly close is often quite different than the stress-inducing swings that take place during the week. Are there exceptions to these rules of thumb? Yes, crisis periods require a bit more monitoring and focus (see 2008).

Focus On Support And Resistance

One way to reduce stress is to say, “I will leave my portfolio alone as long as the market closes above support”. This week is a good example. We have noted reasons to be patient on September 8, September 9, and September 10. As of the close on September 11, the support levels we have been watching remain in play, meaning we have remained in “leave it alone” territory during the recent intraday swings (see chart below).

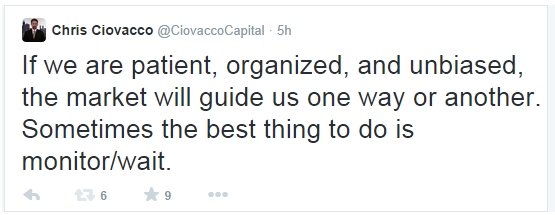

The tweet below from Thursday’s trading session sums up the “when a market is in a range” strategy:

The tweet below from Thursday’s trading session sums up the “when a market is in a range” strategy:

The reference to organization above really speaks to the stress-reducing benefits of systems, rules, and structure.

Friday Is A New Day

Retail sales, consumer sentiment, and business inventories are all on deck. For now, we continue to hold U.S. stocks (SPY), a small stake in bonds (TLT), and leading sectors, such as technology (XLK). Even with the intraday rally Thursday, the S&P 500 is still down 10 points this week. If the bears carry the day Friday, our model may call for an incremental reduction to the growth side of our portfolios. As you might guess, we won’t consider anything firmly until the market nears the close. ~ Chris Ciovacco

This article originally appeared here and was reprinted by permission.

From the editor: Chris is a professional money manager and so he monitors the markets much more than most individuals. Many of us do not monitor our investments on an hourly basis and so the stress of intra-day moves are not a major concern. But some people do monitor the market on a daily or weekly basis and suffer the same stress. The first key to avoiding market stress is not to invest money you will be needing in the short term.

The stock market is ONLY for long term growth. If you will be needing the money in the next year (or five) you don’t want to be concerned about whether the money will be there or not. Unfortunately, with interest rates at historic lows, the alternatives today are all producing very anemic returns. The key though is still to match your time-frame with the investment medium so the money is available when you need it.

Short term money should always be held in “cash equivalents” such as bank accounts, or money market accounts (where the price on one unit is at $1.00 and doesn’t fluctuate). Money that you might need access to in 3 months to 2 years can be held in Certificates of Deposit, Money Market accounts or short term bonds (or bond funds). Money that you won’t need for more than 2 years can be invested carefully in a diversified portfolio that will provide the best overall return (and this is the money Chris is talking about here).

You might also like:

- Deciding Who to Trust With Your Money

- Strategy vs. Tactics in Investing

- Are Annuities for You? Plus 9 Buying Tips

- 1, 2, 3 CD: Saving for the Future

Stress image from Steve Snodgrass via Flickr creative commons.