The Federal Housing Administration (FHA) was created over 80 years ago to help people who do not make a lot of money to be able to afford the American dream of homeownership. About 16 percent of all loans on homes are FHA loans. In order to decide if these loans are right for you, there are several important facts that you will want to consider.

Need a Small down Payment

The average down payment on a conventional loan is 20 percent. Compare that to the down payment on an FHA loan that can be as low as 3.5 percent. The average home in the United States right now sells for $218,000. Therefore, to get an FHA loan one might only need to come up with $7,630 compared to $43,600 for a conventional loan.

Can Have a Lower Credit Score

You can have a lower credit score and qualify for an FHA loan. In fact, you may only need a credit score of 676 compared to a credit score of 767 for a conventional loan. Therefore, if you are now ready to be a responsible homeowner, then you may qualify for a loan even if you were not responsible in the past.

Higher Income-to-Debt Ratio

You can often have a higher income-to-debt ratio and qualify for an FHA loan. In fact, the average person qualifying for FHA home loans has a 29 percent income-to-debt ratio compared to 24 percent for conventional loans. Furthermore, the average person spends 44 percent of their income on recurring debt payments compared to 33 percent for people with conventional loans.

Must Buy Mortgage Insurance

The downside of an FHA loan is that you must buy mortgage insurance. You must buy insurance up front based on approximately 1.75 percent of the home’s selling price. Conventional loans usually require the borrower to carry Private Mortgage Insurance if borrowers don’t provide a minimum 20% down payment. FHA mortgages are different and require the payment of an Up Front Mortgage Insurance Premium and an annual Mortgage Insurance Premium (MIP). Most borrowers have the option to wrap this into their monthly payments, but it is still extra money you have to come up with each month.

If you are dreaming of buying your own home, then an FHA loan may help you reach that dream sooner. The downfall is that it may cost you a little more before you can finally relax with no mortgage to pay. Talk to a mortgage provider today to learn all the details. Your new home may be closer than you think.

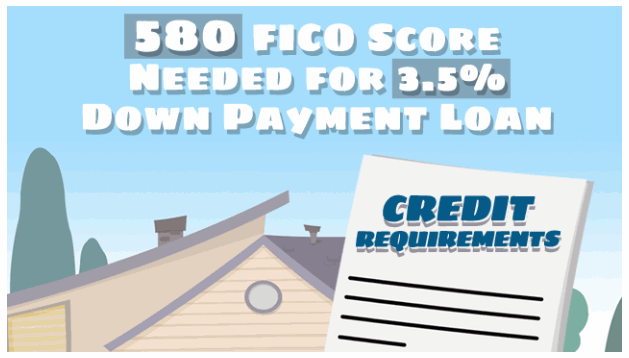

- FICO® score at least 580 = 3.5% down payment.

- FICO® score between 500 and 579 = 10% down payment.

- MIP (Mortgage Insurance Premium ) is required.

- Debt-to-Income Ratio < 43%.

- The home must be the borrower’s primary residence.

- Borrower must have steady income and proof of employment.

You might also like: